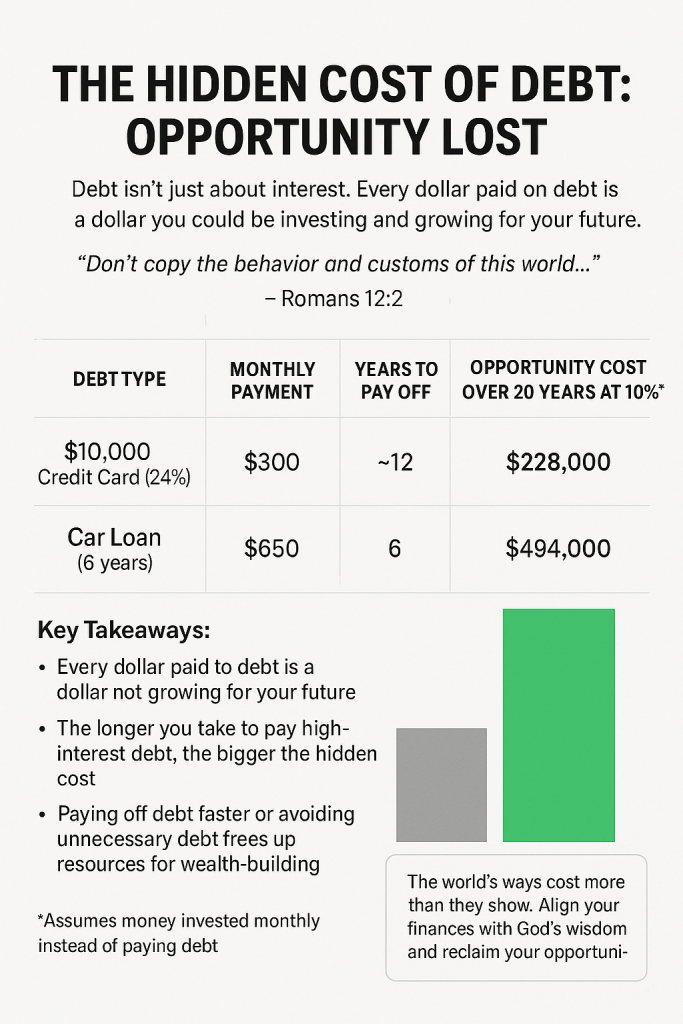

Debt has become a common part of our culture. Mortgages, credit cards, car loans, and personal loans often feel like manageable tools—so much so that they can seem like a normal part of life. Yet the Bible challenges us to think differently. Romans 12:2 says, “Don’t copy the behavior and customs of this world…” In other words, we are called not to follow the patterns of the world blindly, but to allow God’s wisdom to guide our choices.

When it comes to money, this verse has profound implications. Many people focus only on the obvious cost of debt—the interest—but fail to see the hidden cost: the opportunities they sacrifice while making payments. Every dollar spent servicing debt is a dollar that cannot be invested, saved, or used to grow one’s financial future. Over time, the opportunity cost of debt can far exceed the interest itself, limiting your ability to build wealth, prepare for emergencies, or pursue life-giving goals.

By aligning our financial decisions with God’s principles rather than the world’s patterns, we can free ourselves from the hidden burdens of debt and redirect our resources toward opportunities that have lasting value. In this way, financial freedom becomes not just a practical goal, but a spiritual one as well.

Scenario 1: $10,000 Credit Card Debt at 22% Interest, Paying 3% Minimum

As of Q2 2025, average credit card debt per household is around $10,951, while the average interest rate is 22.7%.

Step 1: Monthly minimum payment

3% of $10,000 = $300/month (approximate starting point).

Step 2: Estimate payoff time

Credit cards at high interest can take many years to pay off if paying only minimums. Using the minimum payment formula: =3% of balance, but balance decreases slowly, so average roughly $300.

This will take roughly 10–12 years to pay off the debt, and total interest could be more than $19,000 (much more than the original $10k balance). This is also assuming you don’t add anything to the debt.

Step 3: Opportunity cost over 20 years

Now, suppose instead of paying $300/month to the card, you invested $300/month for 20 years at 10% annual return.

✅ Result: Investing $300/month for 20 years at 10% = ~$228,000.

So the opportunity cost of letting that $10,000 credit card linger and only paying minimums is enormous—over $200k lost potential growth.

Scenario 2: $650 Monthly Car Payment for 6 Years

Step 1: Total payments

- $650 × 12 months × 6 years = $46,800

- Interest portion might be around $5,000–$6,000 depending on rate, so total payments roughly $46k–$47k

Step 2: Opportunity cost over 20 years

Instead of paying $650/month for the car, invest it at 10% for 20 years:

✅ Result: Investing $650/month for 20 years at a 10% return = ~$494,000

So the opportunity cost of tying yourself to a 6-year car loan is nearly half a million dollars in potential growth over 20 years!

Key Takeaways

- High-interest debt grows fast while opportunities for investing grow exponentially.

- Even moderate debt payments, when invested consistently over time, could become substantial wealth.

- This shows why debt isn’t just a financial cost—it’s a massive opportunity cost.